The landscape of life insurance offerings presents a diverse array of options, each designed to meet varying needs and financial objectives. For many individuals contemplating financial security for their loved ones, the choice between different policy types can be a significant undertaking. Among the numerous considerations, a fundamental comparison often emerges: guaranteed issue whole life vs term insurance. These two categories represent distinct approaches to life coverage, differing significantly in their structure, duration, cost, and the underlying principles governing their issuance and benefits.

This guide aims to dissect these differences, providing a neutral and fact-based analysis of each policy type. By exploring their core features, intended purposes, and the circumstances under which they typically apply, readers can gain a more comprehensive understanding. The objective is to shed light on the mechanics of each policy, allowing for an informed perspective on their respective roles in a personal financial strategy.

The Foundations of Life Insurance

Before delving into the specifics of guaranteed issue whole life vs term insurance, it is beneficial to establish a foundational understanding of life insurance as a concept. At its core, life insurance is a contract between an insurer and a policyholder, wherein the insurer promises to pay a designated beneficiary a sum of money upon the insured person’s death. This payment, known as a death benefit, is typically provided in exchange for premiums paid by the policyholder. The primary purpose of life insurance is to provide financial protection and security to dependents or heirs, mitigating the economic impact of an individual’s passing.

Generally, life insurance policies are broadly categorized into two main types: temporary and permanent. Term insurance falls under the temporary category, offering coverage for a specified period. Whole life insurance, including its guaranteed issue variant, is a form of permanent insurance, designed to provide coverage for an individual’s entire lifetime.

Deciphering Term Life Insurance

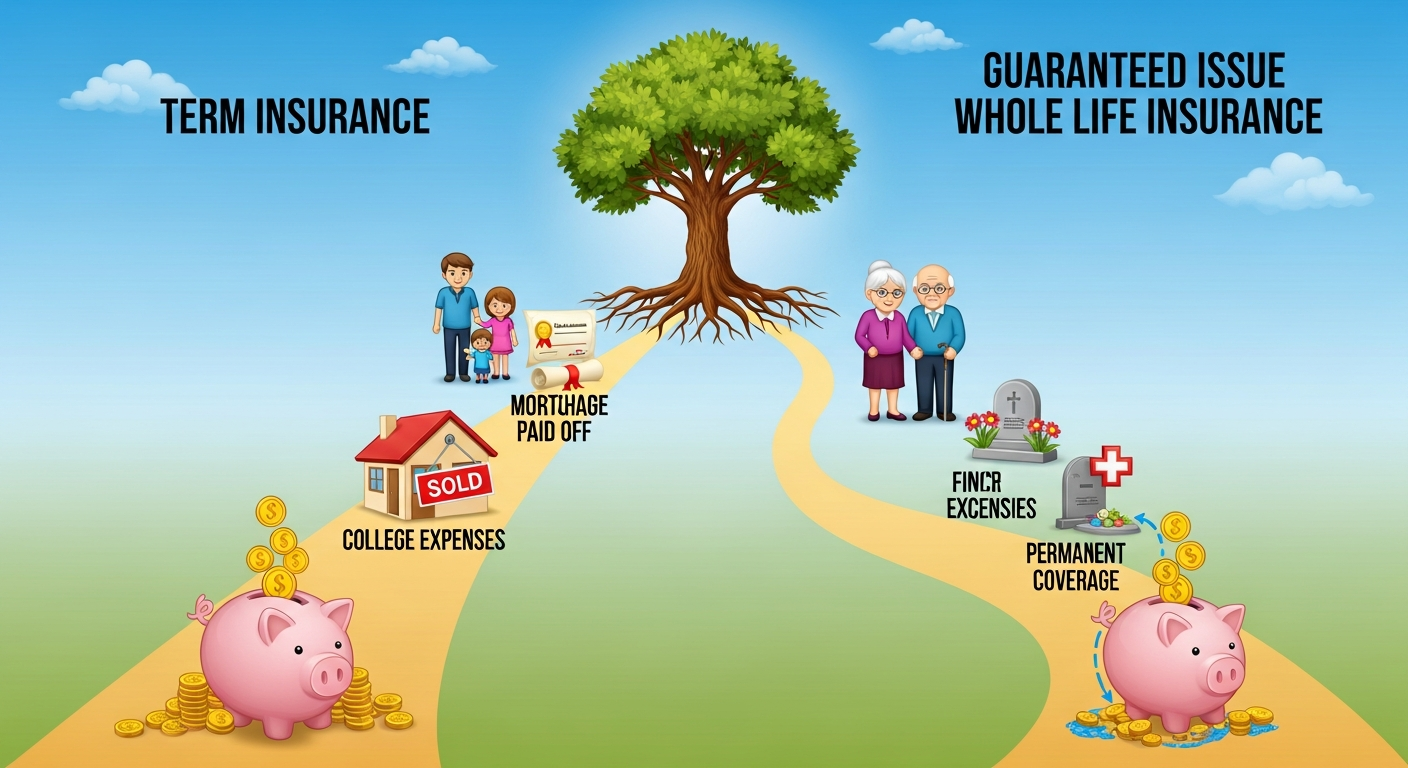

Term life insurance is characterized by its simplicity and defined duration. As its name suggests, it provides coverage for a specific ‘term’ or period, which can range from 5, 10, 20, or even 30 years. If the insured individual passes away within this specified term, the beneficiaries receive the death benefit. If the term expires and the insured is still living, the coverage typically ceases, and no payout is made. Policies may offer options for renewal, often at a higher premium reflecting the insured’s increased age and health risks, or conversion to a permanent policy.

Key Characteristics of Term Life Insurance:

- Fixed Term: Coverage is active only for a predetermined number of years.

- Level Premiums: Premiums usually remain constant throughout the policy term.

- No Cash Value: Term policies do not accumulate a cash value component, meaning they cannot be borrowed against or surrendered for cash.

- Underwriting Process: Standard term life insurance typically involves a thorough underwriting process, including a medical examination and review of health history, which influences eligibility and premium rates.

- Affordability: Generally, term life insurance offers higher coverage amounts for lower premiums compared to permanent life insurance, particularly for younger, healthier individuals.

Common Applications of Term Life Insurance:

Term life insurance is often selected by individuals seeking to cover specific, temporary financial obligations. This might include ensuring income replacement for young families, covering the duration of a mortgage, or safeguarding against business debts that are expected to be retired within a set timeframe. Its cost-effectiveness makes it an accessible option for those needing substantial coverage on a budget, providing peace of mind during critical life stages when financial responsibilities are often at their peak.

Exploring Whole Life Insurance

In contrast to term insurance, whole life insurance is a form of permanent life insurance designed to provide coverage for the entire duration of an individual’s life, as long as premiums are paid. It combines a death benefit with a savings or investment component, known as cash value. The premium structure for whole life policies is typically level, meaning the premiums remain the same for the life of the policy.

Key Characteristics of Whole Life Insurance:

- Permanent Coverage: The policy remains in force for the insured’s entire life.

- Level Premiums: Premiums are fixed and guaranteed not to increase over time.

- Cash Value Accumulation: A portion of each premium payment contributes to a cash value component, which grows on a tax-deferred basis. This cash value can be accessed through policy loans or withdrawals, or it can be surrendered for its cash value.

- Guaranteed Death Benefit: The death benefit is guaranteed as long as premiums are paid.

- Complex Underwriting: Traditional whole life insurance typically involves a comprehensive underwriting process, similar to term life, to assess risk.

Common Applications of Whole Life Insurance:

Whole life insurance is often considered for long-term financial planning objectives, such as estate planning, wealth transfer, or providing lifelong financial security for dependents. The cash value component can also serve as a source of funds for future needs, though accessing it may reduce the death benefit.

Understanding Guaranteed Issue Whole Life Insurance

A specific variant within the whole life category is guaranteed issue whole life insurance. This type of policy stands apart primarily due to its simplified underwriting process. As the name suggests, ‘guaranteed issue’ implies that acceptance is assured for eligible applicants, typically without the need for a medical examination or detailed health questions. This accessibility is its defining characteristic.

Key Characteristics of Guaranteed Issue Whole Life Insurance:

- Guaranteed Acceptance: Most applicants within a specific age range (often 50-85) are accepted, regardless of their health status.

- No Medical Exam: A medical examination is not required, and typically, only a few basic health-related questions are asked, or sometimes none at all.

- Graded Death Benefit: A significant feature of guaranteed issue policies is the graded death benefit. This means that if the insured passes away within the first two or three years of the policy (the ‘waiting period’), the beneficiaries typically receive only the premiums paid, plus a small amount of interest, rather than the full death benefit. The full death benefit usually becomes payable only after this waiting period has passed. In some cases, accidental death during the waiting period may pay the full benefit.

- Higher Premiums: Due to the increased risk taken on by the insurer (as they are accepting applicants without full health assessment), premiums for guaranteed issue policies are generally higher per unit of coverage compared to medically underwritten policies.

- Lower Coverage Amounts: The death benefit amounts offered by guaranteed issue policies are typically lower than those available with traditional term or whole life insurance.

Common Applications of Guaranteed Issue Whole Life Insurance:

Guaranteed issue whole life insurance is predominantly sought by individuals who may have pre-existing health conditions that make them ineligible for traditional life insurance, or for those who simply prefer to avoid the medical examination process. It is often utilized to cover final expenses, such as funeral costs, medical bills, or outstanding debts, providing a measure of financial relief for surviving family members without the burden of extensive health checks.

Direct Comparison: Guaranteed Issue Whole Life vs Term Insurance

The distinction between guaranteed issue whole life vs term insurance is fundamental and impacts their suitability for different financial planning scenarios. A direct comparison reveals their core differences across several key parameters.

Underwriting Process:

- Term Insurance: Typically requires comprehensive medical underwriting, including health questionnaires, medical exams, and review of medical records. This allows insurers to accurately assess risk and offer competitive premiums.

- Guaranteed Issue Whole Life: Characterized by simplified or no underwriting. Acceptance is guaranteed for eligible age groups, making it accessible to those with health challenges. This ease of access, however, comes with implications for cost and benefit structure.

Policy Duration:

- Term Insurance: Offers temporary coverage for a specified number of years (e.g., 10, 20, 30 years). Coverage ends when the term expires, unless renewed or converted.

- Guaranteed Issue Whole Life: Provides permanent coverage that lasts for the insured’s entire lifetime, as long as premiums are paid.

Cash Value Accumulation:

- Term Insurance: Does not build any cash value. It is pure death benefit protection.

- Guaranteed Issue Whole Life: Accumulates a cash value over time, which can be accessed by the policyholder. This accumulation is typically slower and smaller relative to traditional whole life policies due to the higher administrative costs and risk associated with guaranteed issue.

Cost and Premiums:

- Term Insurance: Generally the most affordable type of life insurance for a substantial death benefit, especially for younger, healthier individuals. Premiums are typically level for the term.

- Guaranteed Issue Whole Life: Has significantly higher premiums per dollar of death benefit compared to term insurance, reflecting the insurer’s increased risk due to waiving medical underwriting. Premiums are level for life.

Death Benefit Structure:

- Term Insurance: Provides a full death benefit from the policy’s effective date, assuming all conditions are met.

- Guaranteed Issue Whole Life: Features a graded death benefit, meaning the full death benefit is typically not payable if the insured dies within the first two to three years of the policy. During this initial period, beneficiaries usually receive only a return of premiums paid plus interest.

Purpose and Suitability:

- Term Insurance: Ideal for covering temporary financial needs such as income replacement during child-rearing years, mortgage protection, or specific debt coverage. It provides maximum coverage for the lowest initial cost.

- Guaranteed Issue Whole Life: Best suited for individuals who have difficulty obtaining traditional life insurance due to health issues or advanced age, primarily for covering final expenses like funeral costs, medical bills, or small outstanding debts, ensuring these burdens do not fall to their family. It offers guaranteed acceptance and lifelong coverage, albeit with limitations.

The choice between guaranteed issue whole life vs term insurance therefore hinges on a careful evaluation of an individual’s health status, age, financial objectives, and budget constraints. Neither policy is inherently ‘better’ than the other; rather, their utility is defined by the specific needs they are intended to address.

Factors Influencing the Decision

Making an informed decision about life insurance involves considering several personal and financial factors. When weighing guaranteed issue whole life vs term insurance, the following elements are often central to the deliberation:

Age and Health Status:

For younger, healthier individuals, term insurance often provides the most economical way to secure a large death benefit. The comprehensive underwriting process of term policies allows insurers to offer lower premiums to those with a favorable health profile. Conversely, for older individuals or those with significant health issues, guaranteed issue whole life insurance becomes a relevant option, providing coverage when traditional policies might be inaccessible. Its lack of medical underwriting removes a significant barrier for many.

Financial Objectives and Needs:

The primary financial goal dictates the type of coverage most suitable. If the objective is to protect against a specific, time-bound financial responsibility, such as supporting children through college or paying off a mortgage, term insurance aligns well due to its temporary nature and affordability. If the goal is to ensure funds for final expenses, regardless of when death occurs, and traditional underwriting is a barrier, guaranteed issue whole life insurance offers a practical solution for lifelong coverage.

Budget Constraints:

The cost of premiums is a practical consideration for most individuals. Term insurance generally provides more death benefit per premium dollar, making it a budget-friendly option for high coverage needs. Guaranteed issue whole life insurance, while offering guaranteed acceptance, typically commands higher premiums for comparatively lower death benefits due to the elevated risk assumed by the insurer.

Desire for Cash Value:

The presence of a cash value component is a key differentiator. Term insurance offers no cash value. Whole life policies, including guaranteed issue, build cash value over time. For those who view their life insurance policy as also having a savings or liquidity component, the cash value feature of whole life can be appealing, though it should be noted that the primary purpose of life insurance remains the death benefit.

Future Insurability:

Term policies typically expire, potentially leaving an individual uninsured at an older age or if their health deteriorates. While some term policies offer conversion options to permanent coverage, these conversions usually occur at higher rates. Guaranteed issue whole life insurance, by design, provides permanent coverage, ensuring that once obtained, the policy remains in force for life as long as premiums are maintained, irrespective of future health changes.

The Role of Underwriting in Policy Access and Cost

Underwriting is the process by which an insurer assesses the risk associated with insuring an applicant. This assessment directly influences whether an applicant is approved for coverage and at what premium rate. The differences in underwriting are perhaps the most significant factors distinguishing guaranteed issue whole life vs term insurance.

For standard term life insurance and traditional whole life insurance, the underwriting process is comprehensive. It involves collecting detailed information about an applicant’s medical history, current health, lifestyle (e.g., smoking habits, risky hobbies), and family medical history. This information allows the insurer to categorize the applicant into a risk class, which then determines the premium. Healthier individuals in lower risk classes receive more favorable premium rates.

In contrast, guaranteed issue whole life insurance largely bypasses this extensive process. By accepting nearly all applicants within a certain age bracket, the insurer takes on an undifferentiated risk pool. To compensate for this higher, unknown risk, guaranteed issue policies incorporate mechanisms like the graded death benefit and charge higher premiums per unit of coverage. This trade-off ensures accessibility for those who might otherwise be uninsurable, but at a cost reflective of the increased uncertainty for the insurer.

Understanding the implications of underwriting is critical. For those in good health, pursuing a medically underwritten term policy often yields the most financial efficiency, providing significant coverage for a relatively low cost. For those with compromised health or a strong desire to avoid medical assessments, the guaranteed acceptance of guaranteed issue whole life insurance offers a vital pathway to securing some level of coverage, particularly for final expenses, despite the higher cost and initial benefit limitations.

Conclusion

The choice between guaranteed issue whole life vs term insurance is a nuanced one, reflecting diverse personal circumstances, financial goals, and health profiles. Term insurance offers temporary, cost-effective coverage, primarily for defined periods of significant financial responsibility, typically requiring a medical assessment. It is a straightforward solution for those seeking maximum protection for a limited time at an affordable premium.

Guaranteed issue whole life insurance, on the other hand, provides permanent coverage with guaranteed acceptance, bypassing the need for a medical exam. While it offers invaluable accessibility for individuals with health challenges or those in advanced age, it comes with specific characteristics such as a graded death benefit, higher premiums, and generally lower coverage amounts. Its primary utility often lies in covering end-of-life expenses when other forms of coverage are inaccessible.

Ultimately, a thorough understanding of the distinct features, advantages, and limitations of each policy type is paramount. Informed consideration of one’s own health, financial needs, budget, and long-term objectives will guide individuals toward the type of life insurance coverage that aligns most appropriately with their specific requirements for financial protection and peace of mind.